Skip to content

Skip to navigation

Site map

Official government website

Quick top menu links

Residents

Businesses

Community

Events

News

Departments

Action toolbar

Answers

Payments

Report Issue

Search

City of Bedford, OH

Primary menu links

Public meetings

Parking Snow Ban

City of Bedford, OH

Documents and forms

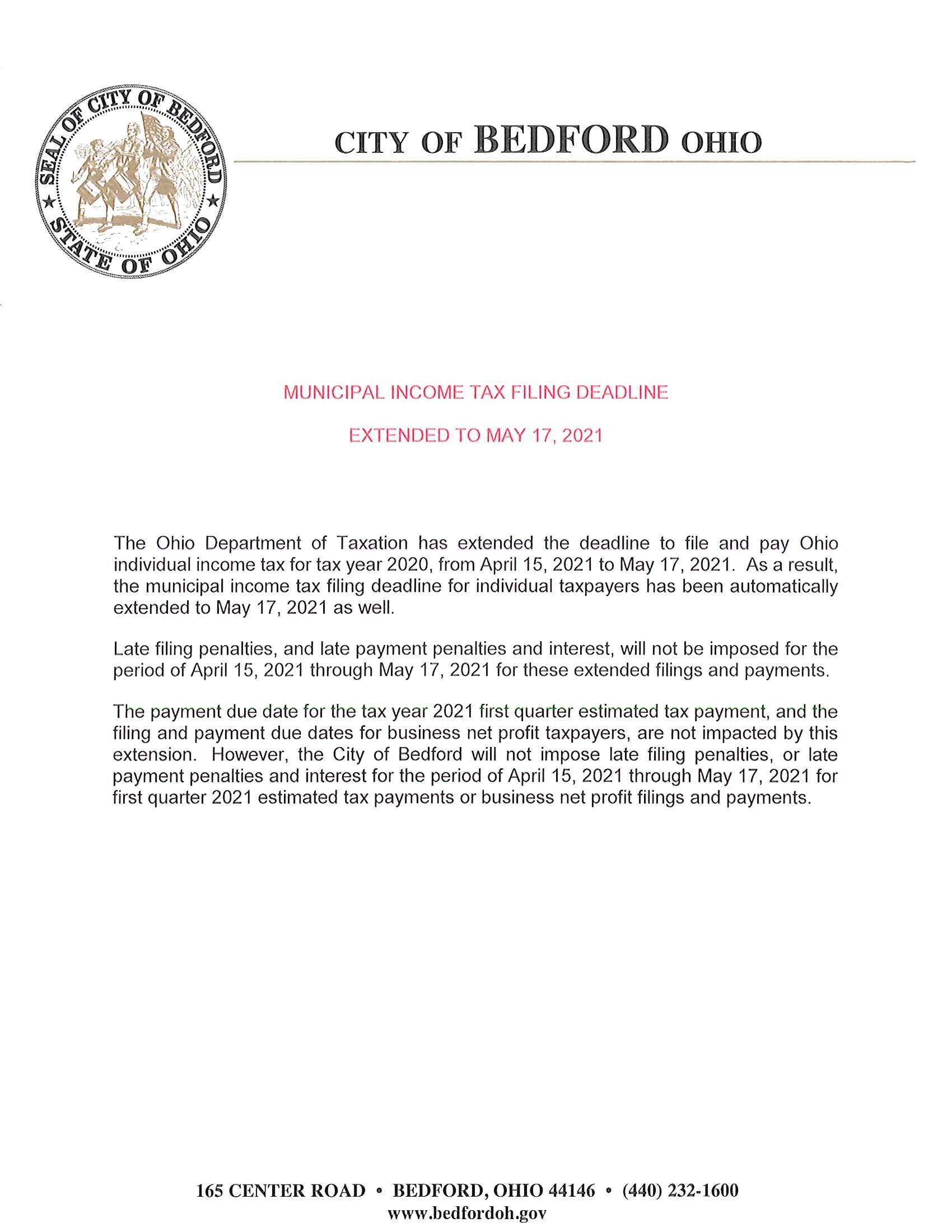

Municipal Income Tax Filing Deadline Extended to May 17, 2021

March 18, 2020

JPG

278 KB

Download

Popout

Helpful

Share

Facebook

Twitter

Email

Size

+

Reset

a

−

Translate

Translate language select

This content is for decoration only

skip decoration

.

Close window

Search Site

Search

Close window

{kind=link}